Hi

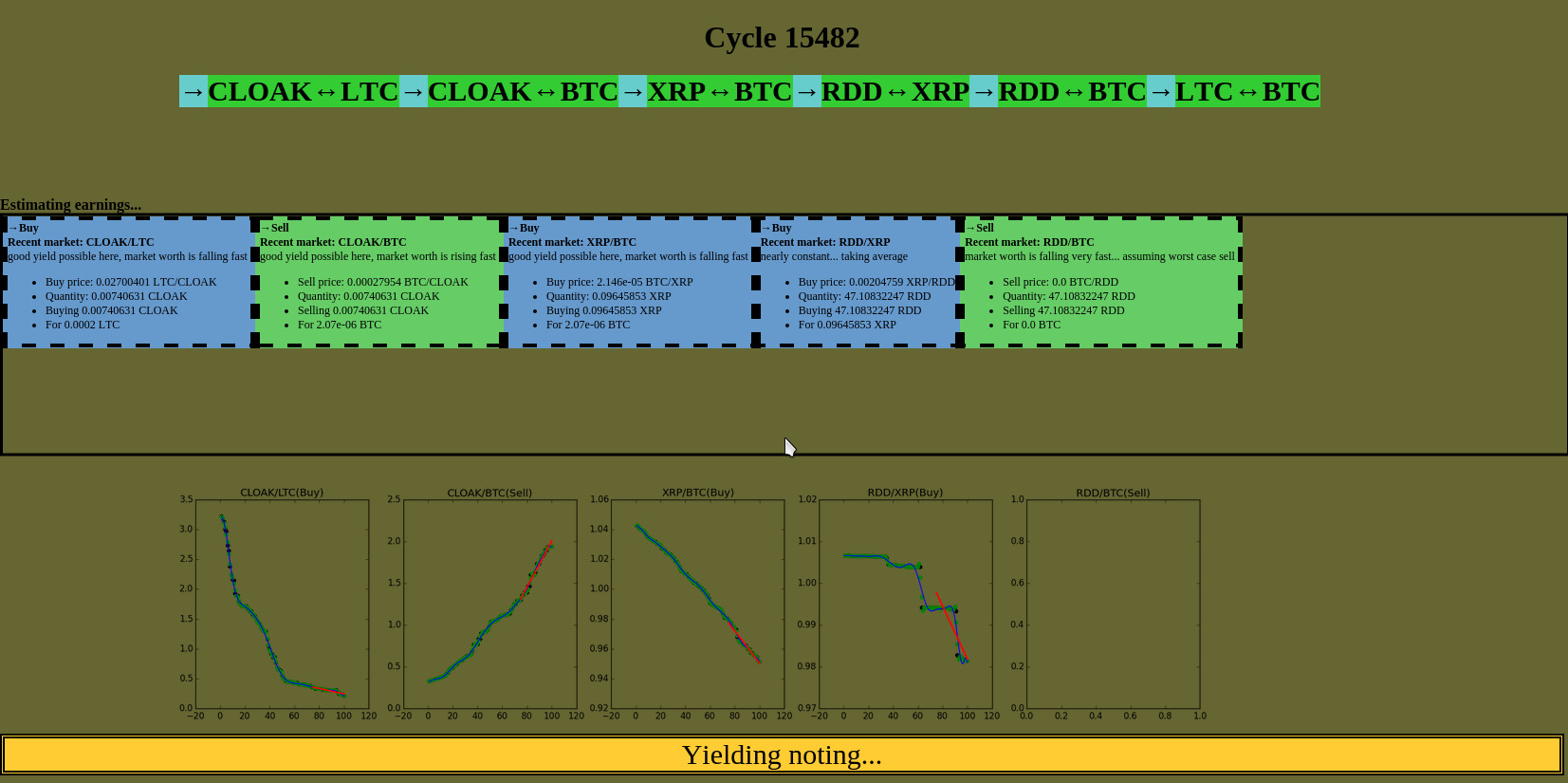

I’m working on a python script which uses a cascaded triangular arbitrash in order to multiply money.

But so far the calculations seem to be all unsatisfying.

What I’m doing so far is fetching and filtering and interpolating the values in order to estimate the trade development:

#!/usr/bin/python

import sys

import os

import copy

import math

# delays:

from time import sleep

# web api

from Cryptsy import Api

#plotting the stuff

import matplotlib

matplotlib.use("TkAgg")

from matplotlib.pyplot import plot

from matplotlib.pyplot import figure

from matplotlib.pyplot import close

from matplotlib.backends.backend_tkagg import FigureCanvasTkAgg, NavigationToolbar2TkAgg

from IPython import display

#numpy stuff:

from numpy import delete

from numpy import array

from numpy import linspace

from numpy import polyfit

from numpy import poly1d

from numpy import newaxis

from numpy import ones

#scipy stuff

from scipy.signal import wiener

from scipy.optimize import curve_fit

from scipy.ndimage.filters import convolve1d

from scipy.interpolate import interp1d

from scipy.interpolate import InterpolatedUnivariateSpline

from scipy.signal import wiener

from scipy.signal import gaussian

from scipy.signal import savgol_filter

#sklearn

from sklearn.gaussian_process import GaussianProcess

from sklearn.linear_model import LinearRegression

from sklearn.isotonic import IsotonicRegression

from sklearn.cross_validation import cross_val_predict

from sklearn.preprocessing import PolynomialFeatures

from sklearn.pipeline import Pipeline

from sklearn.utils import check_random_state

#pyqt fit

from pyqt_fit import npr_methods

import pyqt_fit.nonparam_regression as smooth

…

x = linspace(1, len(price_array), len(price_array)) y = array(price_array) filtered_y = savgol_filter(y, window_length, savgol_filter_polyorder) k0 = smooth.NonParamRegression(x, filtered_y, method=npr_methods.LocalPolynomialKernel(q=gauss_poly_deg)) k0.fit() z = k0(x) avg_diff_number=len(x)/4 new_x=x[len(x)-avg_diff_number-1:] new_z=z[len(z)-avg_diff_number-1:] clf = LinearRegression() clf.fit(new_x[:,newaxis],new_z) tangent=clf.predict(new_x[:,newaxis]) num_different=(tangent[-1]-tangent[0])/(new_x[-1]-new_x[0])

If someone has a better idea: Please say so!

maybe The Application of Echo State Network in Stock Data

Mining” Lin et al. 2008?